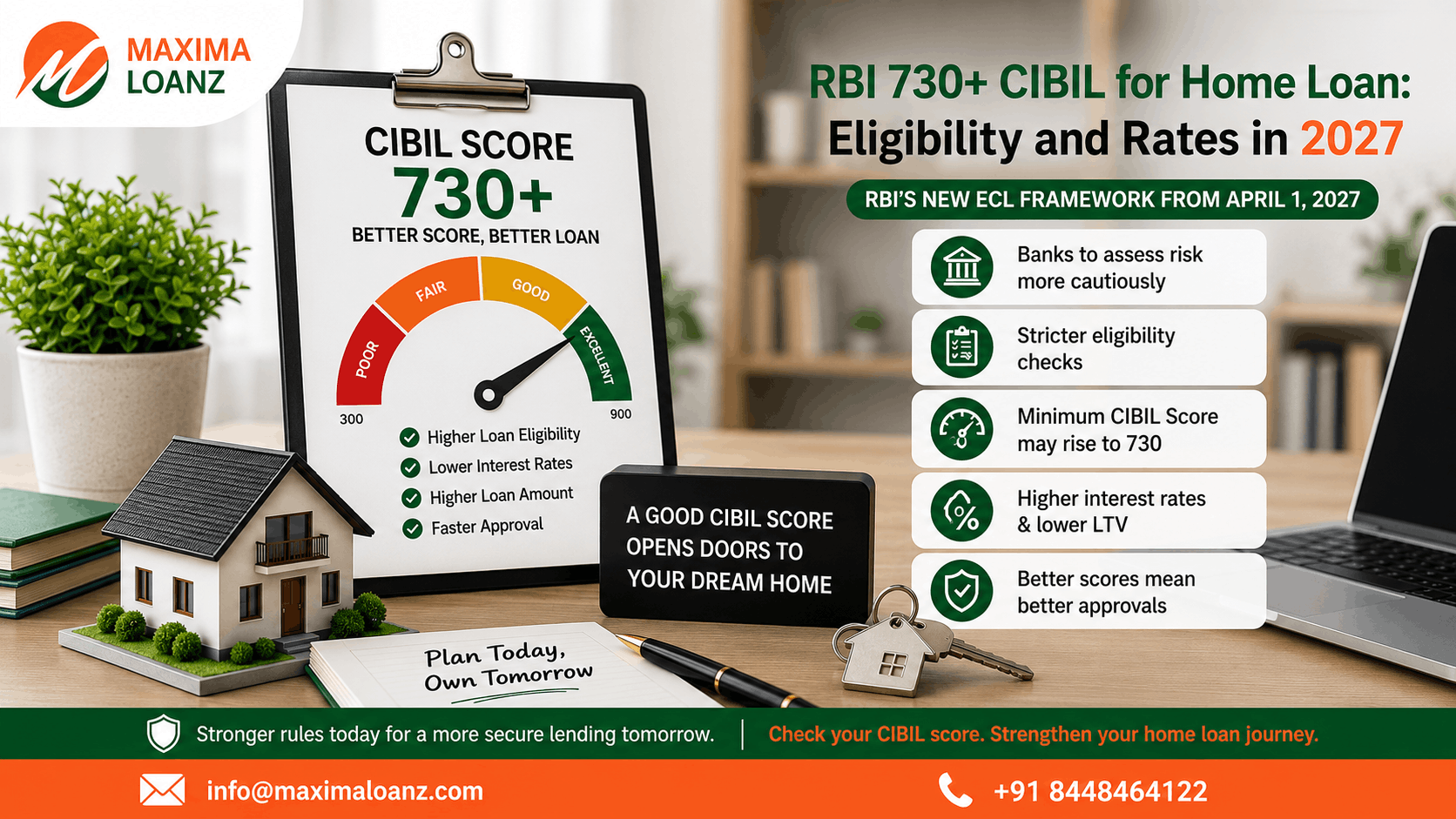

If you are planning to apply for a home loan in the coming years, your CIBIL score will become more important than ever.

The Reserve Bank of India (RBI) plans to implement the ‘Expected Credit Loss’ (ECL) framework on April 1, 2027. Consequently, banks may scrutinize the eligibility of home loan applicants much more rigorously. This could lead to stricter eligibility criteria and a closer examination of repayment histories, alongside a potential increase in the minimum required CIBIL score to 730.

Read this blog to understand how this new rule will impact your home loan application, the minimum CIBIL score requirement, and your existing loans.

What are the Effects on Home Loans After New Changes?

Many homeowners are wondering whether the new changes proposed by the RBI will impact their home loan applications. Based on these proposed changes, banks may alter the terms for both mortgage applications and loan sanctions to curb non-performing assets (NPAs). Unlike previous regulations, the new guidelines suggest that banks should be able to forecast potential losses from bad loans and determine the necessary reserve funds for the RBI. Consequently, banks might adjust interest rates, CIBIL score eligibility criteria, and loan-to-value (LTV) ratios to mitigate the risk of loss and weed out borrowers likely to default.

The RBI’s new measures could affect home loan applications and CIBIL score requirements.

730+ CIBIL Required, Home Loan Eligibility Gets Tougher

According to the latest ECL guidelines, the minimum CIBIL score required to obtain a home loan must be above 730. Unlike earlier standards, a credit score of 700–720 may not be sufficient to secure a home loan. Banks are likely to scrutinize your credit score more rigorously, and if any issues are found in your repayment history, they may deny the loan. Even if your CIBIL score is 730+, you might only be able to secure a loan at higher interest rates. The new norms also mandate that banks monitor your CIBIL and credit scores even after the loan has been sanctioned.

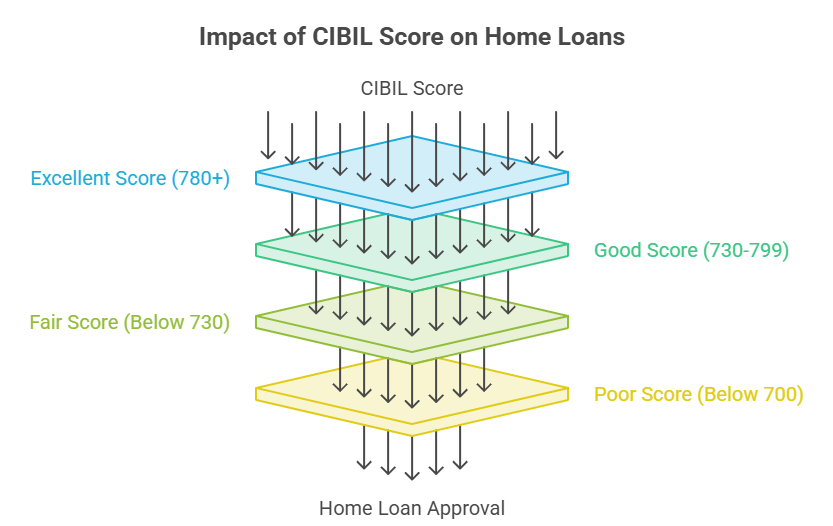

| CIBIL Score | Impact of RBI’s ECL Framework on Home Loan |

| 780+ | Better interest rates, faster loan approval, and higher home loan eligibility. |

| 730-799 | Standard interest rates, stricter financial scrutiny, and possible impact on the sanctioned loan amount. |

| Below 730 | Higher interest rates, increased chances of loan rejection, and a larger down payment may be required. |

| Below 700 | Very low chances of home loan approval from most banks. |

Changes in Interest Rate Calculation: One Interest Won’t Fit-All

New RBI guidelines could impact the way banks determine interest rates on home loans. For FY28, home loans continue to be based on an ‘all-inclusive’ interest rate system. However, recent changes may lead to various adjustments. Previously, banks offered the same interest rate on home loans to all borrowers; now, to mitigate the risk of losses arising from loan defaults, they may offer higher interest rates to individuals with lower CIBIL scores.

Possible Revision in Loan-to-Value (LTV) Ratio

The portion of a property’s value that banks lend to homebuyers is known as the ‘Loan-to-Value’ (LTV) ratio. If the new ECL standards are fully implemented, banks might offer lower LTV ratios.

For instance, under current regulations, banks typically offer an LTV of 85–90 percent when you take out an investment loan for a home. If your house is valued at ₹50 lakh, the bank would provide a loan ranging from ₹35 lakh to ₹40 lakh. Once the ECL framework is implemented, banks may offer you a lower LTV option based on factors such as your credit score, income, and other parameters.

What is the RBI’s ECL Framework?

The ‘Expected Credit Loss’ (ECL) framework is a forward-looking model for loan provisioning. It helps banks mitigate risk before loans actually default or turn into Non-Performing Assets (NPAs). Under this model, the RBI directs banks to assess potential losses in advance and set aside funds (make provisions) for them. All banks currently utilize this model. In contrast, the ‘Incurred Loss Model’ focuses on assessing loans that are already underperforming and then taking appropriate action. While ECL is a predictive model, the ‘Incurred Loss Model’ is reactive rather than proactive, addressing losses only after they have occurred.

Therefore, the RBI mandates that all banks implement this new model, enabling them to anticipate losses, categorize them, and take precautionary measures before the losses materialize.

Impact on Secured vs Unsecured Loan

Secured loans are based on collateral, whereas unsecured loans are not affected by collateral. The modern structure of such loans may yield some results. The impact on secured loans such as mortgages and car loans may be less as banks can recover the loan amount by taking possession of the collateral. However, unsecured loans can vary widely as they do not require collateral and are higher risk.

The interest rate offered for home loans can range from 0.25% to 0.50% overall, depending on loan repayment history, credit history, type of default and job stability. Unlike a secured loan, the amount of provision can range from 1% to 3% depending on several factors.

Impact on Freelancers and Gig Workers

Following the RBI’s new guidelines on home loans, freelancers and gig workers may face an increased risk of having their loan applications rejected. This is because their income can be volatile or irregular, potentially leading financial institutions to view them as likely loan defaulters.

What Can You Do to Minimize Its Effects?

You can adopt certain measures to mitigate the negative impact of the ECL framework on your home loan application:

- Do not apply if your credit score is low, as a home loan rejection can lower your credit rating.

- The ECL framework is designed to encourage financial discipline; therefore, avoid missing repayments or over-borrowing. Pay off existing debts and make a larger down payment before applying to improve your chances of securing the loan.

- Ensure you have a stable income to avoid falling into the second stage of the ECL framework.

Apply Home Loan with Maxima for Smooth Home Loan Journey

The RBI’s new ECL framework could transform the way loans are availed and disbursed in India. That is why we encourage you to enhance your financial literacy, enabling you to make informed decisions throughout your financial journey. If you are planning to take out a home loan, ensure you are well-informed about all the necessary details before applying. At Maxima, we can assist you with the latest updates and changes regarding home loans, help you find the best lender, and facilitate the loan process. As India’s most trusted home loan consultants, we can help you navigate the impact of the ECL regulations. Contact us today to elevate your home loan experience.

Frequently Asked Questions

Ques. Does RBI require a 730+ CIBIL score for home loans?

Ans. No. RBI does not prescribe a minimum CIBIL score for home loans. Individual banks and lenders set their own credit score requirements based on their lending policies.

Ques. Is a 730 CIBIL score good for a home loan?

Ans. Yes. A CIBIL score of 730 is generally considered good and can improve your chances of home loan approval while helping you qualify for better interest rates.

Ques. Can I get a home loan with a CIBIL score below 730?

Ans. Yes. Many lenders approve home loans for borrowers with scores below 730, although the interest rate may be higher and additional eligibility checks may apply.

Ques. How can I improve my CIBIL score before applying for a home loan?

Ans. Pay EMIs and credit card bills on time, keep your credit utilization low, avoid multiple loan applications in a short period, and regularly review your credit report for errors.